Financial Literacy Is a Life Skill, Not an Elective by Karin Humbolt

- Karin Humbolt

- Apr 25

- 3 min read

Most adults can remember a class they took in school that they never used again. But there is one class most of us never took that we use every single day for the rest of our lives: how to manage money. Financial literacy is not an elective. It is a life skill. And the cost of waiting until adulthood to learn it is enormous.

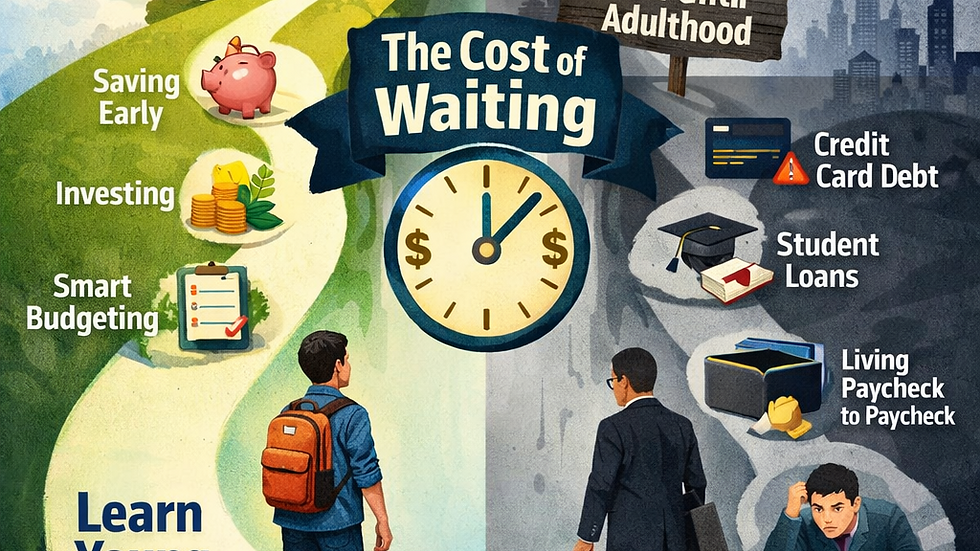

The Cost of Waiting Until Adulthood

By the time many young adults learn about money, they have already signed student loan agreements, opened credit cards, financed cars, and made spending decisions that will affect them for years. They are making adult financial decisions with a teenager’s financial education.

When financial literacy is delayed until adulthood, people often learn through mistakes instead of education. Credit card debt, high-interest loans, poor budgeting, and lack of savings are not just financial problems — they are life problems. They affect career choices, stress levels, relationships, and future opportunities.

The earlier someone understands money, the more time they have to make smart decisions instead of expensive mistakes.

Time Is the Most Powerful Financial Tool

Teenagers have something incredibly valuable that adults no longer have: time. Time allows money to grow through compound interest. Time allows for mistakes to be small and recoverable. Time allows good habits to become lifelong habits.

A teenager who understands saving, investing, and debt before their first paycheck is years — even decades — ahead of someone who learns the same lessons at age 30.

Financial education is not about getting rich quickly. It is about understanding how money works so that time can do the heavy lifting.

Financial Decisions Start Earlier Than Parents Think

Many people think financial education should start in college. In reality, financial decisions start much earlier:

First job

First car

First debit card

First online purchases

First student loan decision

First credit card offer

If a teenager does not understand interest, debt, budgeting, and saving before these moments, they are learning while the stakes are high.

We do not wait until someone is in a car accident to teach them how to drive. We should not wait until someone is in debt to teach them how money works.

Financial Literacy Is a Workforce Skill

Financial literacy is also a career skill. Young adults entering the workforce are expected to make decisions about:

Salary offers

Employee benefits

Health insurance

Retirement plans

Taxes

Cost of living

Relocation decisions

Yet many have never been taught how to read a paycheck, how a 401(k) works, or how to build a budget based on income.

Financial literacy helps young people not only earn money, but keep it and grow it.

A Life Skill, Not an Elective

We require students to take math, science, and history. But money will impact a person’s life every month, every year, for their entire life. Few subjects have a more direct impact on a person’s quality of life than how they manage their money.

Financial literacy is not about raising rich kids. It is about raising independent adults who understand how to earn, save, spend, and invest wisely.

The best time to teach financial literacy is not after college, or after debt, or after financial mistakes.

The best time to teach financial literacy is while people are still young enough for the knowledge to change their future.

Because when teenagers understand money, they don’t just change their finances — they change their life trajectory.

Comments